Humana Medicare Supplement Insurance Plans: Navigating the world of Medicare can feel like deciphering ancient hieroglyphs, but understanding supplemental plans doesn’t have to be a headache. This deep dive into Humana’s offerings reveals the ins and outs of their various plans – from the budget-friendly to the bells-and-whistles options. We’ll break down the costs, coverage, and even the sneaky fine print, so you can choose the plan that’s right for *you* without feeling overwhelmed.

We’ll cover everything from the differences between Plan A and Plan G, to how your age and location impact your premiums. We’ll also compare Humana to other big names in the Medicare supplement game, so you can confidently make the best decision for your healthcare needs. Think of us as your friendly neighborhood Medicare Sherpas, guiding you through the sometimes-confusing terrain of supplemental insurance.

Humana Medicare Supplement Plan Overview: Humana Medicare Supplement Insurance Plans

Navigating the world of Medicare can feel like traversing a dense jungle, but understanding Humana’s Medicare Supplement plans can help clear the path to better healthcare coverage. These plans, also known as Medigap plans, help fill the gaps in Original Medicare (Parts A and B), offering extra financial protection against healthcare costs. They’re designed to make healthcare more affordable and less stressful.

Humana offers a range of Medigap plans, each with its own set of benefits and premiums. Choosing the right plan depends on your individual needs and budget. Understanding the differences between these plans is crucial to making an informed decision.

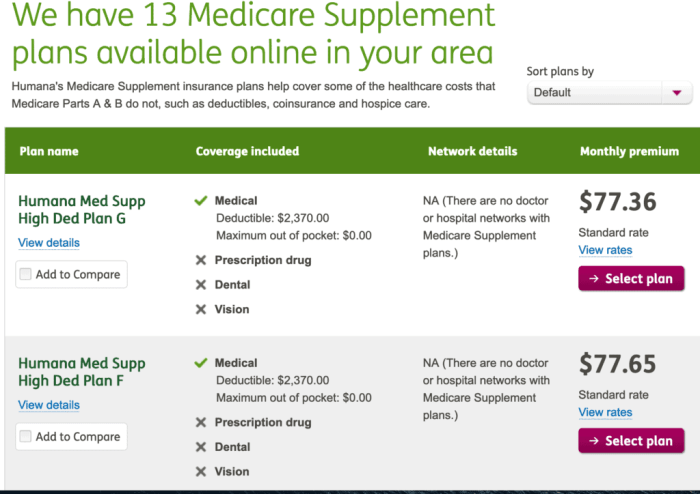

Humana Medicare Supplement Plan Types and Features

Humana offers several Medicare Supplement plans, each designated by a letter (A, G, N, etc.). These plans adhere to standardized benefits as defined by federal regulations, meaning a Plan A from Humana will offer the same core benefits as a Plan A from another insurer. However, premiums can vary. Key differences usually lie in the specific coverage details and, of course, the cost. While all plans help cover Medicare’s cost-sharing amounts, some plans cover more than others. For example, Plan A typically covers the Medicare Part A deductible, while Plan G might cover both Part A and Part B deductibles.

Comparison of Humana Medicare Supplement Plans

The following table compares three common Humana Medicare Supplement plans, highlighting their key features, monthly premium ranges, and limitations. Remember that premiums vary based on age, location, and other factors. It’s always best to get a personalized quote from Humana.

| Plan Name | Key Features | Monthly Premium Range (Example) | Limitations |

|---|---|---|---|

| Plan A | Covers Part A hospital costs (deductible and coinsurance), and some Part B costs. | $100 – $200 | Does not cover Part B deductible or excess charges. |

| Plan G | Covers Part A hospital costs (deductible and coinsurance), Part B costs (deductible and coinsurance), and foreign travel emergency care. | $250 – $400 | Does not cover Medicare Part B excess charges. |

| Plan N | Covers Part A hospital costs (deductible and coinsurance), Part B costs (deductible and coinsurance). | $150 – $300 | Has a copay for some Part B doctor visits and emergency room visits. |

Plan Costs and Coverage

Navigating the world of Medicare Supplement plans can feel like wading through a swamp of jargon and fine print. Understanding the costs and what’s actually covered is crucial to choosing a plan that fits your budget and healthcare needs. Let’s break down the key factors that influence the price tag and the specifics of what each plan covers.

Several factors significantly impact the monthly premium you’ll pay for a Humana Medicare Supplement plan. Your age is a major player – older individuals generally pay more due to a statistically higher likelihood of needing more healthcare services. Your location also matters; premiums can vary considerably from state to state, reflecting differences in healthcare costs and provider networks. Finally, while Humana doesn’t use your health status to determine eligibility for a Medicare Supplement plan, your individual health needs could indirectly influence your costs. For example, if you anticipate needing extensive medical care, a plan with broader coverage might be worth the higher premium.

Factors Influencing Plan Costs

The interplay of age, location, and individual health needs creates a complex pricing structure. For instance, a 65-year-old in Florida might pay a different premium than a 75-year-old in New York, even if they choose the same plan type. This is because healthcare costs, administrative expenses, and state regulations all contribute to the final premium. Understanding these variations is essential for making an informed decision.

Illustrative Plan Cost Variations

The table below provides a hypothetical illustration of how these factors can influence monthly premiums. Remember, these are estimates and actual costs will vary based on the specific plan, your individual circumstances, and the current market rates. Always check with Humana for the most up-to-date pricing information.

| Age Group | Location | Plan Type (Example) | Estimated Monthly Premium |

|---|---|---|---|

| 65-69 | Florida | Plan G | $150 |

| 70-74 | Florida | Plan G | $200 |

| 65-69 | New York | Plan G | $180 |

| 70-74 | New York | Plan G | $250 |

Medicare Supplement Plan Coverage

Humana offers various Medicare Supplement plans (often referred to as Medigap plans), each offering different levels of coverage. Understanding the nuances of each plan is crucial. While all Medigap plans must adhere to standardized benefits as defined by the federal government, the specific aspects of coverage can vary. For example, some plans cover Part A and Part B deductibles, while others might only cover Part B coinsurance.

Generally, a higher premium equates to more comprehensive coverage. However, this doesn’t automatically mean the most expensive plan is the best for everyone. Your individual healthcare needs and budget should guide your choice. It’s essential to carefully review the specific benefits included in each plan to determine which best suits your circumstances. For example, Plan A is generally the most affordable, offering basic coverage, while Plan F (no longer sold to those under 65) historically offered the most comprehensive coverage, but this is no longer the case with recent changes to Medicare Supplement plans.

Navigating Humana Medicare Supplement insurance plans can feel like a maze, but understanding your options is key to a secure retirement. For those in the construction industry, however, securing the right protection extends beyond retirement; finding the best workers comp insurance for construction is crucial for on-the-job safety. Back to Humana, remember that choosing the right Medicare plan is just as vital for your long-term well-being.

Enrollment and Eligibility Requirements

Source: seniorliving.org

Navigating the world of Medicare Supplement plans can feel like deciphering a complex code, but understanding the enrollment process and eligibility requirements is key to securing the coverage you need. This section clarifies the process, making it easier to understand and navigate.

Eligibility for Humana Medicare Supplement plans hinges primarily on your Medicare status. You must be enrolled in both Medicare Part A (hospital insurance) and Part B (medical insurance) to be eligible for a Medigap plan. There are specific enrollment periods that impact your options, and understanding these is crucial for securing the best possible coverage. Certain pre-existing conditions may also affect your eligibility or the cost of your plan.

Medicare Eligibility

To enroll in a Humana Medicare Supplement plan, you must first be enrolled in Medicare Part A and Part B. Part A generally covers hospital stays, while Part B covers doctor visits and other medical services. Your eligibility for Part A and B is determined by your age and work history (or that of your spouse). Individuals who are 65 or older and meet certain work history requirements are typically eligible for both parts. Those under 65 may also qualify for Medicare due to certain disabilities or specific medical conditions. Confirming your eligibility for Medicare Parts A and B is the foundational step before considering a Medigap plan.

Enrollment Process

The enrollment process for Humana Medicare Supplement plans is straightforward, but requires attention to detail. You’ll need to gather specific documentation and complete an application. While the process may vary slightly depending on your specific circumstances, understanding the general steps involved can streamline the experience.

- Review Plan Options: Carefully compare Humana’s various Medigap plans to determine which best fits your needs and budget. Consider factors like coverage levels and premiums.

- Gather Required Documents: This typically includes your Medicare card, driver’s license or other identification, and potentially other documentation depending on your situation. Humana will specify exactly what you need during the application process.

- Complete the Application: Fill out the application accurately and completely. Double-check all information for accuracy to avoid delays or complications.

- Submit Application and Documentation: Submit your completed application and all necessary documentation to Humana. You can often do this online, by mail, or over the phone.

- Review Your Policy: Once Humana approves your application, carefully review your policy to ensure everything is correct and that you understand the terms and conditions.

Required Documentation

The specific documents required for enrollment can vary slightly, but generally include proof of Medicare enrollment (your Medicare card), identification (driver’s license or state-issued ID), and possibly other supporting documentation. Humana will Artikel the exact requirements during the application process. It’s crucial to have all necessary documentation readily available to expedite the application process. Failure to provide complete and accurate documentation can lead to delays in processing your application.

Comparing Humana to Competitors

Source: medicarehope.com

Choosing a Medicare Supplement plan can feel like navigating a maze. Understanding the differences between major providers like Humana, AARP, and UnitedHealthcare is crucial for making an informed decision. This section compares Humana’s offerings to those of its key competitors, focusing on plan types, key features, and average monthly premiums to help you weigh your options effectively.

Direct comparison across all plans and regions is difficult due to varying plan structures and regional pricing. Premium costs are highly dependent on age, location, and the specific plan chosen. The data presented below represents averages based on publicly available information and should be considered a general guideline, not a precise reflection of individual costs.

Medicare Supplement Plan Comparison

The table below provides a simplified comparison of Humana’s Medicare Supplement plans against those offered by AARP and UnitedHealthcare. Remember that specific plan details and pricing can vary significantly by location and individual circumstances. Always check with the individual insurers for the most up-to-date information.

| Provider | Plan Type | Key Features | Average Monthly Premium* |

|---|---|---|---|

| Humana | Plan G, Plan N | Comprehensive coverage (Plan G), lower premiums (Plan N with co-pays), strong provider network | $150 – $300 |

| AARP (UnitedHealthcare) | Plan G, Plan F (in limited areas) | Wide network access, strong reputation, potentially lower premiums in certain regions | $140 – $280 |

| UnitedHealthcare | Plan G, Plan N, other supplemental plans | Variety of plan options, strong provider network, potentially specialized benefits | $130 – $290 |

*Average monthly premium is a hypothetical range and will vary based on location, age, and specific plan details. This is not a guarantee of pricing.

Humana’s Strengths and Weaknesses

Humana boasts a large provider network and offers a range of Medicare Supplement plans, including popular options like Plan G and Plan N. Their customer service is generally well-regarded, although individual experiences may vary. However, Humana’s premiums might be higher in certain areas compared to competitors like AARP or UnitedHealthcare, particularly for certain plan types. Furthermore, the breadth of their supplemental plans might be less extensive than UnitedHealthcare’s in some regions.

Customer Reviews and Ratings

Understanding what real Humana Medicare Supplement plan users think is crucial before making a decision. Customer reviews offer a valuable, unfiltered perspective supplementing official plan details. Analyzing both positive and negative feedback helps paint a complete picture of the customer experience.

Several reputable sources, including AARP, Medicare.gov, and independent review sites, provide access to customer reviews and ratings. While star ratings offer a quick summary, reading individual reviews reveals valuable insights into specific plan aspects, such as customer service responsiveness, claims processing speed, and the overall clarity of the plan’s information.

Positive Customer Experiences

Many positive reviews highlight Humana’s customer service representatives’ helpfulness and responsiveness. Users frequently praise the ease of filing claims and the speed of processing. The extensive network of doctors and hospitals accepted by Humana plans is also frequently cited as a major advantage.

- “The customer service representatives were incredibly helpful and patient in answering all my questions. They made the entire process stress-free.”

- “My claim was processed quickly and efficiently. I received payment within days.”

- “I was able to see my preferred doctor without any issues. The network of providers is excellent.”

Negative Customer Experiences

Conversely, some negative reviews criticize Humana’s customer service for long wait times and difficulties reaching a representative. Complaints regarding the complexity of plan details and the lack of clarity in certain aspects are also common. In some cases, issues with claim denials and slow processing times have been reported.

- “I spent hours on hold trying to reach customer service. When I finally got through, the representative wasn’t very helpful.”

- “The plan’s details were confusing, and I had difficulty understanding what was covered.”

- “My claim was denied, and the reason given was unclear. The appeals process was also very difficult.”

Potential Hidden Costs and Fine Print

Source: cloudinary.com

Navigating the world of Medicare Supplement plans can feel like wading through a swamp of jargon and fine print. While Humana’s Medicare Supplement plans offer comprehensive coverage, it’s crucial to understand the potential hidden costs and limitations that might not be immediately obvious during the initial sales pitch. Failing to do so could lead to unexpected out-of-pocket expenses down the line. Let’s shed some light on these often-overlooked aspects.

Understanding these less-apparent aspects of Humana’s Medicare Supplement plans is key to making an informed decision and avoiding financial surprises. Remember, the devil is in the details, and a thorough understanding of the fine print can save you significant money and headaches in the long run.

Premium Increases

Humana, like other insurance providers, reserves the right to increase premiums annually. While the initial premium might seem attractive, it’s essential to consider the potential for future increases, especially as you age. These increases can be substantial and significantly impact your budget over time. For example, a plan with a seemingly low initial premium might see a 10% or even higher increase within a year or two, drastically altering your monthly expenses. It’s advisable to carefully review the company’s history of premium increases and consider the potential long-term financial implications.

Limitations on Specific Services

While Humana’s Medicare Supplement plans offer broad coverage, certain services may have limitations or exclusions. For instance, some plans might have limits on the number of days covered for rehabilitation or skilled nursing care. Others may impose restrictions on the types of providers you can see or the specific treatments covered. Carefully review the policy’s detailed benefit schedule to understand these nuances. For example, a plan might cover 80% of the cost of physical therapy, but only up to a certain number of visits per year.

Pre-existing Conditions

While Medicare Supplement plans generally cover pre-existing conditions after a waiting period, the specifics of this coverage can vary. Understanding the waiting period for pre-existing conditions is vital. A longer waiting period means you’ll be responsible for more out-of-pocket costs during that time. Humana’s policy details regarding pre-existing conditions should be thoroughly reviewed before enrollment. For instance, a pre-existing condition like diabetes might have a longer waiting period than a less severe condition.

Network Restrictions

Although many Medicare Supplement plans don’t have strict networks like HMOs, some Humana plans may offer additional benefits or discounts for using in-network providers. While you’re not typically *required* to use in-network providers, doing so might lead to cost savings or better access to care. Understanding these nuances is important for budgeting and planning your healthcare. Failing to utilize in-network providers, if available, could lead to higher out-of-pocket expenses.

Out-of-Pocket Maximums

While Medicare Supplement plans aim to minimize out-of-pocket costs, they often have out-of-pocket maximums. Once you reach this limit, the plan covers 100% of eligible expenses. However, understanding the amount of this maximum is crucial. A higher out-of-pocket maximum means you could potentially face substantial expenses before the plan takes over the full cost of your care. For example, a plan with a $5,000 out-of-pocket maximum could still leave you with significant expenses if you experience a serious illness or injury.

- Premium Increases: Annual premium increases are common and can significantly impact long-term costs.

- Limitations on Specific Services: Certain services may have limitations on coverage, such as the number of visits or types of providers.

- Pre-existing Condition Waiting Periods: There may be waiting periods before coverage for pre-existing conditions begins.

- Network Restrictions (Potential Cost Savings): Using in-network providers may lead to cost savings, but is not always mandatory.

- Out-of-Pocket Maximums: Understanding the plan’s out-of-pocket maximum is essential to budgeting for healthcare expenses.

Understanding the Claims Process

Navigating the claims process for your Humana Medicare Supplement plan might seem daunting, but with a clear understanding of the steps involved, it becomes much more manageable. This section breaks down the process, offering a step-by-step guide to ensure a smooth and efficient experience. Remember, prompt action and accurate documentation are key to a quick resolution.

Filing a claim with Humana for your Medicare Supplement plan involves several straightforward steps. The process is designed to be user-friendly, but having a clear understanding beforehand will save you time and potential frustration. Humana offers multiple ways to submit claims, catering to various preferences and technological comfort levels.

Submitting a Claim

To submit a claim, you’ll need to gather the necessary documentation. This typically includes your Humana member ID card, the provider’s bill, and any other relevant medical records. You can then choose to submit your claim through one of several methods: online through your Humana account, by mail using the provided claim form, or by fax. Humana’s website and member materials provide detailed instructions and the necessary forms for each method. Be sure to keep copies of all submitted documents for your records.

Claim Processing Timeline, Humana medicare supplement insurance plans

Humana aims to process claims efficiently. The processing time can vary depending on the complexity of the claim and the completeness of the submitted documentation. While Humana provides estimated processing times on their website, it’s best to allow a reasonable timeframe for processing. If you haven’t heard back within a reasonable period (check Humana’s website for their specified timeframe), contacting their customer service department is recommended.

Claim Status Tracking

Tracking the status of your claim is easy. You can typically do this online through your Humana member account. This online portal provides real-time updates on your claim’s progress, allowing you to monitor its journey from submission to completion. This feature significantly reduces uncertainty and keeps you informed throughout the process.

Example Claim Process Flowchart

The following bullet points illustrate a typical claim process:

* Step 1: Obtain Medical Services: Receive medical care from a participating provider.

* Step 2: Receive Provider’s Bill: Get the bill from your healthcare provider.

* Step 3: Gather Necessary Documentation: Collect your Humana member ID card and any supporting medical documents.

* Step 4: Choose a Submission Method: Decide to submit your claim online, by mail, or by fax.

* Step 5: Submit Your Claim: Complete and submit your claim using your chosen method.

* Step 6: Claim Processing: Humana processes your claim, verifying information and eligibility.

* Step 7: Payment (or Denial): Humana either processes the payment to your provider or sends a denial letter with reasons for denial.

* Step 8: Review Denial (If Applicable): If denied, review the reasons for denial and decide whether to appeal.

* Step 9: Appeal (If Necessary): Follow Humana’s appeal process if you disagree with the denial.

Customer Service and Support

Navigating the world of Medicare supplements can be confusing, so having reliable customer service is crucial. Humana, a major player in the Medicare Advantage and Supplement market, offers various ways to get in touch, but the quality of their service is a frequently discussed topic among consumers. Understanding their support channels and the general experiences of their customers is key to making an informed decision.

Understanding Humana’s customer service options is important for a smooth experience with your Medicare Supplement plan. Their accessibility and responsiveness directly impact your ability to address questions, resolve issues, and manage your coverage effectively.

Humana’s Customer Service Channels

Humana provides several avenues for contacting their customer service representatives. These options cater to different preferences and levels of technological comfort. The ease of access and speed of response can vary depending on the method chosen.

| Contact Method | Description |

|---|---|

| Phone | Humana offers a dedicated phone number for Medicare Supplement plan inquiries. Wait times can vary depending on the time of day and demand. Representatives are generally available during standard business hours. Expect to provide your policy number and other identifying information. |

| Online | Their website provides a portal for accessing account information, submitting claims, and finding answers to frequently asked questions (FAQs). Live chat support may be available during certain hours. The online portal allows for self-service options, reducing the need to call. |

| Written correspondence can be sent to a designated Humana address. This method is generally the slowest, with response times often taking several business days or even longer. It is suitable for non-urgent matters or formal requests. |

Humana Customer Service Reputation and Responsiveness

Customer reviews and ratings regarding Humana’s customer service are mixed. While many report positive experiences with helpful and knowledgeable representatives, others cite long wait times, difficulty reaching a live person, and frustrating resolution processes. Online forums and review sites often reveal a range of experiences, highlighting the importance of individual circumstances and expectations. For example, some users praise the online resources, while others find the website cumbersome to navigate. The responsiveness of Humana’s customer service seems to depend on factors such as the complexity of the issue, the time of day, and the chosen contact method. Independent ratings agencies often provide aggregated scores based on customer feedback, which can be useful in assessing overall performance.

Final Conclusion

Choosing a Medicare Supplement plan is a big deal, but it doesn’t have to be a stressful one. By understanding the nuances of Humana’s plans – the costs, the coverage, and the potential pitfalls – you can confidently select a plan that fits your budget and your healthcare needs. Remember, doing your research is key to making an informed decision that protects your financial well-being and peace of mind in your golden years. So, grab your magnifying glass (metaphorically speaking!), and let’s make sure you’re getting the best bang for your buck.

{kind=link}