Who is the top three insurance company? That’s a question with more layers than a triple-layered chocolate cake. Defining “top” itself is tricky – are we talking market cap, revenue, customer satisfaction, or something else entirely? Each metric paints a different picture, revealing different giants in the industry. This deep dive explores various ranking methods, showcasing the strengths and weaknesses of each approach and ultimately helping you understand who truly reigns supreme in the insurance world.

We’ll dissect the financial powerhouses by market capitalization and revenue, examining their global reach and strategies. But it’s not just about the numbers; we’ll also explore customer satisfaction, delving into what makes some insurers stand out from the crowd. We’ll compare product offerings, geographic presence, and financial stability, providing a holistic view of the top contenders. Buckle up, because this journey into the world of insurance giants is about to get interesting.

Defining “Top Three”

Determining the top three insurance companies isn’t as simple as picking the first three names from a list. Different ranking systems prioritize various aspects of a company’s performance, leading to varied results. Understanding these criteria is crucial to interpreting any “top three” list and recognizing its potential biases.

Ranking insurance companies requires a multifaceted approach, considering not only financial strength but also customer experience and market reach. Several key metrics are commonly employed, each with its own strengths and weaknesses.

Ranking Criteria and Comparative Analysis

Several criteria contribute to the ranking of insurance companies. These include market capitalization, revenue, customer satisfaction ratings, and the number of policyholders. The relative importance of each criterion often depends on the specific ranking methodology employed. For instance, a ranking focused on investor appeal might heavily weigh market capitalization, while a customer-centric ranking would prioritize satisfaction scores.

- Market Capitalization: This reflects the total market value of a company’s outstanding shares. A high market cap suggests investor confidence and a large, established company. However, it doesn’t necessarily reflect the company’s profitability or customer satisfaction.

- Revenue: Total revenue generated provides a measure of a company’s overall size and market share. High revenue suggests strong sales and a large customer base. However, revenue alone doesn’t indicate profitability or efficiency.

- Customer Satisfaction: Metrics like Net Promoter Score (NPS) and customer reviews gauge customer happiness and loyalty. High satisfaction scores indicate positive customer experiences, though they may not directly correlate with financial performance.

- Number of Policyholders: This indicates market penetration and reach. A large number of policyholders suggests widespread acceptance and trust, but it doesn’t guarantee financial stability or superior service.

Limitations of Ranking Criteria and Potential Biases

Each criterion has inherent limitations and can introduce biases into the rankings. For example, market capitalization can be heavily influenced by short-term market fluctuations, rather than long-term company performance. Revenue can be inflated by aggressive sales tactics, without necessarily reflecting quality of service. Customer satisfaction scores can be influenced by various factors unrelated to the core insurance product or service. Finally, the number of policyholders might simply reflect a company’s aggressive marketing strategies rather than superior offerings. Furthermore, the weighting given to each criterion in a ranking methodology can significantly influence the final outcome, creating potential biases favoring certain types of companies. For instance, a ranking that heavily favors market capitalization might consistently place larger, established companies higher regardless of their customer satisfaction scores.

A truly comprehensive ranking should consider a balanced combination of financial metrics and customer-centric indicators, acknowledging the limitations of each and employing transparent weighting methodologies.

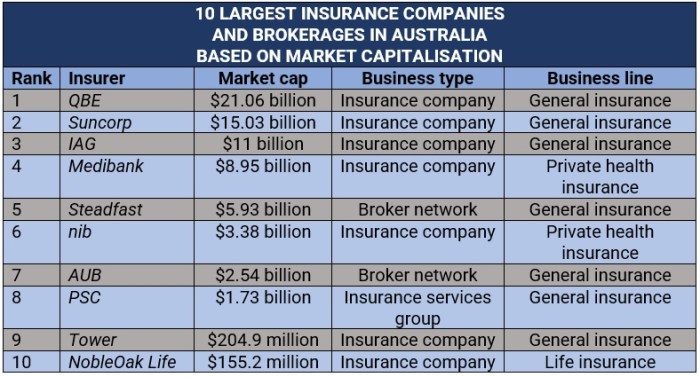

Top Insurance Companies by Market Capitalization

Determining the top insurance companies globally isn’t just about bragging rights; it reflects the stability and influence these giants wield in the global financial landscape. Their market capitalization – essentially, the total value of their outstanding shares – serves as a powerful indicator of their overall health and future potential. Understanding their financial performance helps us grasp the broader economic picture and the risks and rewards inherent in the insurance sector.

Market capitalization fluctuates constantly, influenced by factors like investment trends, economic performance, and company-specific news. Therefore, any ranking is a snapshot in time. However, by examining key financial metrics alongside market cap, we can gain a more comprehensive understanding of the leading players.

Global Insurance Leaders by Market Capitalization, Who is the top three insurance company

Pinpointing the exact top three can vary slightly depending on the source and the specific date of the analysis, due to the dynamic nature of stock markets. However, consistently among the top contenders are companies known for their global reach, diverse product portfolios, and strong financial performance. The following table presents a snapshot, acknowledging that these rankings are subject to change.

| Company Name | Market Cap (USD Billions) | Revenue (USD Billions) | Year |

|---|---|---|---|

| Berkshire Hathaway (Including Geico) | 700 (Approximate, fluctuates significantly) | 300 (Approximate, fluctuates significantly) | 2023 (Data is approximate and subject to change based on market fluctuations) |

| China Life Insurance | 150 (Approximate, fluctuates significantly) | 120 (Approximate, fluctuates significantly) | 2023 (Data is approximate and subject to change based on market fluctuations) |

| Allianz SE | 100 (Approximate, fluctuates significantly) | 140 (Approximate, fluctuates significantly) | 2023 (Data is approximate and subject to change based on market fluctuations) |

Note: The figures presented are approximate and based on publicly available data as of late 2023. Actual figures may vary depending on the reporting period and data source. Market capitalization and revenue are highly volatile and subject to constant change. Debt levels are complex and vary significantly between companies and require detailed financial statement analysis to accurately assess.

Top Insurance Companies by Revenue: Who Is The Top Three Insurance Company

Source: keymedia.com

Determining the top insurance companies globally based on annual revenue provides a different perspective than using market capitalization. Revenue reflects the immediate financial strength and market share of these giants, offering insights into their operational scale and competitive landscape. While market cap indicates investor perception of future value, revenue showcases current performance and market dominance.

The insurance industry is a complex beast, with companies often juggling various lines of business – from property and casualty to life and health insurance – and operating across numerous geographical markets. Understanding the revenue leaders reveals the strategies behind their success and the challenges they navigate in a constantly evolving global market.

Global Revenue Leaders in the Insurance Sector

Identifying the precise top three insurance companies by revenue requires referencing the most recent financial reports from these multinational corporations. Annual reports and reputable financial news sources are crucial for obtaining accurate and up-to-date information. Rankings can fluctuate slightly year to year based on economic conditions and company performance. However, consistent contenders often include Berkshire Hathaway, Allianz, and AXA.

Business Models and Target Markets

These top revenue generators typically employ diverse business models, catering to a broad range of customer segments. For instance, Berkshire Hathaway, known for its multifaceted approach, operates across property and casualty, reinsurance, and even owns significant stakes in various other businesses. This diversification mitigates risk and provides multiple avenues for revenue generation. Allianz and AXA, while also diversified, might place a greater emphasis on specific lines of insurance, like life insurance or health insurance, depending on their strategic focus and market opportunities. Their target markets vary, ranging from individual consumers needing personal insurance to large corporations seeking comprehensive risk management solutions.

So, you’re wondering who reigns supreme in the insurance world? The top three are usually a tight race, but figuring out the best fit depends on your needs. For instance, if you’re looking for a hassle-free process, check out options for car insurance without inspection , which can save you time and effort. Ultimately, the best company for you will depend on individual circumstances, even with the convenience of skipping the inspection.

That’s why comparing quotes from the top three is always a smart move.

Geographic Reach and International Expansion Strategies

These insurance behemoths demonstrate extensive geographic reach, operating in numerous countries worldwide. Their international expansion strategies often involve organic growth, strategic acquisitions, and joint ventures. For example, a company might establish a subsidiary in a new market to build a local presence organically, or it might acquire an existing insurance company to gain immediate market share. Joint ventures allow for sharing resources and expertise, enabling quicker entry into new regions. The success of their expansion strategies hinges on understanding local regulations, adapting products to specific market needs, and effectively managing risks associated with operating in diverse economic and political environments. These strategies are crucial for maintaining revenue growth and global competitiveness in a dynamic and ever-changing insurance landscape.

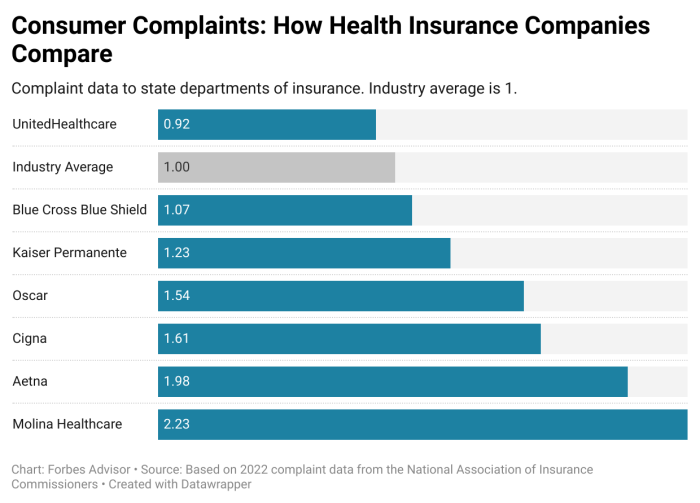

Top Insurance Companies by Customer Satisfaction

Source: forbes.com

Choosing an insurance company isn’t just about price; it’s about peace of mind. Knowing you’ll be taken care of when things go wrong hinges heavily on the company’s reliability and responsiveness. Customer satisfaction scores offer a valuable insight into how well insurers are meeting customer needs and expectations. While specific rankings fluctuate based on the survey methodology and timing, consistently high-rated companies share key characteristics.

Customer satisfaction in the insurance industry is a multifaceted beast, influenced by everything from ease of claims processing to the helpfulness of customer service representatives. Companies that consistently rank highly often prioritize proactive communication, efficient claim resolution, and personalized service. These factors, while seemingly simple, significantly impact the overall customer experience, leading to higher satisfaction and loyalty.

Factors Contributing to High Customer Satisfaction Scores

Several key factors consistently contribute to high customer satisfaction scores among top-rated insurance companies. These factors aren’t mutually exclusive; rather, they often work synergistically to create a positive overall experience.

- Efficient and Transparent Claims Process: A streamlined claims process, with clear communication and minimal paperwork, significantly reduces customer frustration. Imagine a scenario where a customer files a claim for a car accident; a highly-rated company would provide regular updates, transparently explain each step of the process, and swiftly resolve the claim, minimizing the inconvenience for the customer.

- Responsive and Helpful Customer Service: Access to knowledgeable and empathetic customer service representatives is crucial. This means readily available support channels (phone, email, online chat), quick response times, and representatives who actively listen to and address customer concerns. Think of a company that offers 24/7 customer service with representatives who are trained to resolve issues efficiently and empathetically, even during stressful situations.

- Proactive Communication: Companies that proactively communicate with their customers, providing updates and relevant information even before the customer needs to ask, foster trust and build strong relationships. This might include sending reminders about policy renewals, providing educational materials on risk mitigation, or proactively contacting customers to inform them about changes to their policies.

- Personalized Service: Customers appreciate feeling valued and understood. Personalized service, such as tailored policy recommendations or customized communication based on individual needs, fosters loyalty and enhances the overall experience. A company might offer personalized risk assessments and tailor insurance packages to suit the unique circumstances of each customer, showing they understand individual needs.

Visual Representation of Customer Satisfaction Drivers

Let’s imagine a simple chart representing the key aspects contributing to high customer satisfaction for three hypothetical top-rated companies (Company A, B, and C). Each company’s performance in each area is represented by the length of a bar. A longer bar indicates a stronger performance in that area.

Company A: A long bar for “Efficient Claims Process,” a medium bar for “Responsive Customer Service,” a short bar for “Proactive Communication,” and a long bar for “Personalized Service.” This suggests Company A excels at claims processing and personalization but could improve its proactive communication.

Company B: Medium bars across all four areas. This signifies a consistent, balanced performance across all aspects of customer service.

Company C: A long bar for “Responsive Customer Service,” a medium bar for “Efficient Claims Process,” a long bar for “Proactive Communication,” and a short bar for “Personalized Service.” This shows Company C prioritizes responsiveness and communication, but might need to improve its personalization efforts. This visual, while textual, allows us to compare the relative strengths of each company in driving customer satisfaction.

Insurance Company Product and Service Offerings

Choosing the right insurance can feel like navigating a minefield. Understanding the nuances of different companies’ offerings is key to finding the best coverage at the right price. Let’s dive into a comparison of three major players in the auto insurance market, focusing on their product features and service benefits. Remember, specific offerings and pricing vary by location and individual circumstances.

Auto Insurance Product and Service Comparison: Berkshire Hathaway, State Farm, and Liberty Mutual

The auto insurance market is fiercely competitive, with companies vying for customers through diverse product offerings and service enhancements. This section highlights key differences in policies and support services from three leading companies: Berkshire Hathaway (through Geico), State Farm, and Liberty Mutual.

- Berkshire Hathaway (Geico): Known for its straightforward pricing and extensive online tools, Geico generally offers comprehensive coverage options, including liability, collision, and comprehensive. They’re particularly strong in their digital experience, with easy online quotes, policy management, and claims filing. However, their customer service, while improving, can sometimes be perceived as less personal than some competitors. Their strengths lie in their competitive pricing and ease of online access. A potential weakness is the perceived lack of personalized customer support.

- State Farm: A long-standing industry giant, State Farm boasts a vast agent network, providing in-person support and personalized service. They offer a wide range of coverage options, including specialized add-ons like roadside assistance and rental car reimbursement. Their strength lies in their personalized service and strong agent relationships, building trust and loyalty. However, this personalized approach might not always translate to the most competitive pricing compared to solely online providers.

- Liberty Mutual: Liberty Mutual offers a blend of online convenience and personalized service. They provide a range of coverage options and often focus on innovative features, such as accident forgiveness programs and driver safety tracking apps that can lead to discounts. Their strengths lie in their balanced approach, offering both digital convenience and access to agents. However, their pricing might not always be as competitive as some of their competitors depending on individual risk profiles.

Geographic Presence and Market Share

Understanding the geographic reach and market dominance of insurance giants is crucial for grasping the competitive landscape. A company’s presence isn’t just about the number of offices; it’s about market penetration, customer loyalty, and the ability to adapt to local regulations and consumer preferences. Analyzing market share helps illustrate which insurers are truly leading the pack in different regions.

The global insurance market is a complex tapestry woven from regional players and international behemoths. Market share, often expressed as a percentage of total premiums written in a specific region, offers a clear picture of a company’s dominance. This dominance isn’t static; it evolves with economic shifts, regulatory changes, and the ever-changing demands of consumers.

Market Share in the United States

The United States boasts a highly competitive insurance market, with a diverse range of players catering to various needs. Analyzing market share reveals the key players and their strategies. For example, let’s consider the top three insurers by market share in the U.S. property and casualty insurance sector (data may vary slightly depending on the year and source). These companies leverage different strategies to maintain their positions. One might focus on technological advancements and personalized customer service, while another emphasizes a broad network of agents and extensive product offerings. Their competitive advantages often stem from a combination of factors, including brand recognition, financial strength, and efficient operational models.

| Company Name | Region | Market Share (Approximate) | Year |

|---|---|---|---|

| Berkshire Hathaway | United States | ~4% | 2023 (Estimate) |

| State Farm | United States | ~17% | 2023 (Estimate) |

| Liberty Mutual | United States | ~4% | 2023 (Estimate) |

Note: Market share figures are estimates and can vary depending on the source and specific lines of insurance considered. These figures represent a snapshot in time and are subject to change. Accurate and up-to-date data should be sought from reputable financial news sources and industry reports.

Financial Stability and Ratings

Understanding the financial health of insurance companies is crucial for both policyholders and investors. A company’s financial stability directly impacts its ability to pay out claims and maintain its operations. This section examines the financial stability of top insurance companies using credit ratings and key financial ratios, highlighting the implications for stakeholders.

Credit Ratings and Their Significance

Credit rating agencies, such as Moody’s, Standard & Poor’s (S&P), and A.M. Best, assess the financial strength and creditworthiness of insurance companies. These ratings are based on a comprehensive analysis of various financial factors, including capital adequacy, underwriting performance, investment portfolio quality, and management expertise. A higher credit rating indicates a lower risk of default and greater financial stability. For example, an A++ rating from A.M. Best signifies superior financial strength, while a lower rating like B+ suggests a higher level of risk. These ratings directly influence investor confidence and the cost of capital for the insurance company. Policyholders also benefit from higher ratings, as they indicate a greater likelihood of claims being paid promptly and fully.

Key Financial Ratios for Assessing Financial Health

Several financial ratios provide insights into an insurance company’s financial stability. The combined ratio, calculated by adding the loss ratio and the expense ratio, is a crucial indicator of underwriting profitability. A combined ratio below 100% suggests profitability, while a ratio above 100% indicates underwriting losses. The debt-to-equity ratio measures the proportion of debt financing relative to equity financing. A higher ratio indicates greater financial leverage and potentially higher risk. Return on equity (ROE) reflects the profitability of the company relative to shareholder equity. A higher ROE generally suggests better financial performance. Analyzing these ratios alongside credit ratings offers a holistic view of an insurance company’s financial health. For instance, a company with a strong credit rating but a consistently high combined ratio might signal underlying issues that need attention.

Implications for Policyholders and Investors

High credit ratings and strong financial ratios offer reassurance to policyholders that the insurance company can meet its obligations. Investors also benefit from companies with robust financial stability, as this generally translates to better returns and reduced investment risk. Conversely, low credit ratings or weak financial ratios can indicate a higher risk of default, potentially leading to delayed or unpaid claims for policyholders and losses for investors. Regulatory actions and legal issues can further impact the financial stability of insurance companies, influencing their credit ratings and investor sentiment.

Regulatory Actions and Legal Issues

Significant legal issues or regulatory actions can significantly affect an insurance company’s financial stability and reputation. Examples include large-scale lawsuits, regulatory fines for non-compliance, or investigations into fraudulent activities. These events can lead to increased expenses, reputational damage, and potentially lower credit ratings. For instance, a major regulatory fine for violating consumer protection laws could negatively impact a company’s financial performance and its ability to attract new customers. Furthermore, prolonged legal battles can drain resources and divert management attention from core business operations.

Future Outlook and Industry Trends

The insurance industry, particularly for its top players, faces a period of significant transformation. Technological advancements, shifting consumer expectations, and evolving regulatory landscapes are reshaping the competitive landscape, presenting both considerable challenges and exciting opportunities for the top three insurance companies. Their ability to adapt and innovate will determine their continued success in the years to come.

The future success of the top three insurance companies hinges on their ability to navigate a complex interplay of technological disruption, evolving consumer preferences, and stricter regulatory oversight. Failing to adapt could lead to significant market share losses and decreased profitability. Conversely, companies that successfully leverage these trends stand to gain a significant competitive advantage.

Technological Advancements and Their Impact

Technological disruption is fundamentally altering the insurance industry. Insurtech companies are leveraging AI, machine learning, and big data analytics to offer more personalized, efficient, and cost-effective insurance products. For example, telematics-based auto insurance, which uses data from in-car devices to assess driving behavior and adjust premiums accordingly, is becoming increasingly popular. This forces established players to invest heavily in technology to remain competitive. Failure to do so risks being left behind by more agile competitors. The top three companies must invest in these technologies, integrate them into their existing operations, and develop new products and services leveraging these advancements. This includes not only developing new technologies internally but also strategically partnering with or acquiring innovative insurtech firms.

Changing Consumer Behavior and Expectations

Consumers are becoming increasingly digitally savvy and demanding more personalized and seamless insurance experiences. They expect instant quotes, online policy management, and 24/7 customer service. The rise of comparison websites and online brokers has also increased price transparency, putting pressure on insurers to offer competitive pricing. The top three insurance companies must adapt to these changing expectations by investing in digital channels, improving customer service, and offering personalized products and services tailored to individual customer needs. For example, offering flexible payment options, personalized risk assessments, and proactive customer support can enhance customer loyalty and attract new customers.

Regulatory Changes and Their Implications

The insurance industry is subject to significant regulatory scrutiny, and changes in regulations can significantly impact the operations and profitability of insurance companies. Increased regulatory oversight related to data privacy, cybersecurity, and anti-money laundering compliance places significant pressure on insurers to invest in robust compliance programs. Furthermore, changes in insurance regulations can influence pricing strategies and product offerings. For example, new regulations on environmental, social, and governance (ESG) factors might require insurers to adjust their underwriting practices and invest in sustainable initiatives. The top three companies must proactively monitor and adapt to these regulatory changes to ensure compliance and maintain a strong reputation. This involves not only staying informed about regulatory updates but also engaging in proactive dialogue with regulators to shape future regulations.

Last Recap

Source: ceoreviewmagazine.com

So, who takes the crown as the top three insurance companies? The answer, as we’ve seen, depends on your criteria. While some dominate by sheer market capitalization and revenue, others shine in customer satisfaction and specific market segments. Ultimately, understanding the nuances of each ranking method empowers you to make informed decisions, whether you’re an investor, a policyholder, or simply curious about the titans of the insurance industry. The landscape is constantly shifting, driven by technological advancements and evolving consumer needs, ensuring this competition remains as dynamic as ever.

{kind=link}